23 / 56

23 / 56

23

CenSES annual report 2015

Zero-Emission platform (ZEP)

After previously modelling the lowest-cost route for

decarbonising Europe’s power sector, ZEP has in this report

turned its attention to the industry. With direct industry-

related emissions accounting for a quarter of EU’s total CO2

emissions, it is clear that Europe must look beyond the power

sector and likewise include core industries such as refining,

steel and cement. CCS is the only option for substantially

reducing CO2 emissions in these industries. Also the costs of

CO2 transport and storage,10-30% of the total CCS costs, can

be significantly reduced by clustering power and industrial

emitters. Power production alone accounts for a third of

Europe’s GHG emissions, with a single power plant emitting

~1-5 million tonnes of CO2 every year.

In order to realistically study the development of the power

system, including the effect of intermittent renewable

power production and deployment of storage, the EMPIRE

model corporates both strategic and operational decisions

andcosts . The developed model has the following key

features illustrated: (See table 2).

1. Costs of investment in new generation capacity in each

node and year

2. Costs of investment in new storage capacity, divided into

power and energy.

3. Operative costs of generation including the cost of

running generators, emitting CO2 as well as capturing and

transporting the CO2

4. Operative costs due to load shedding.

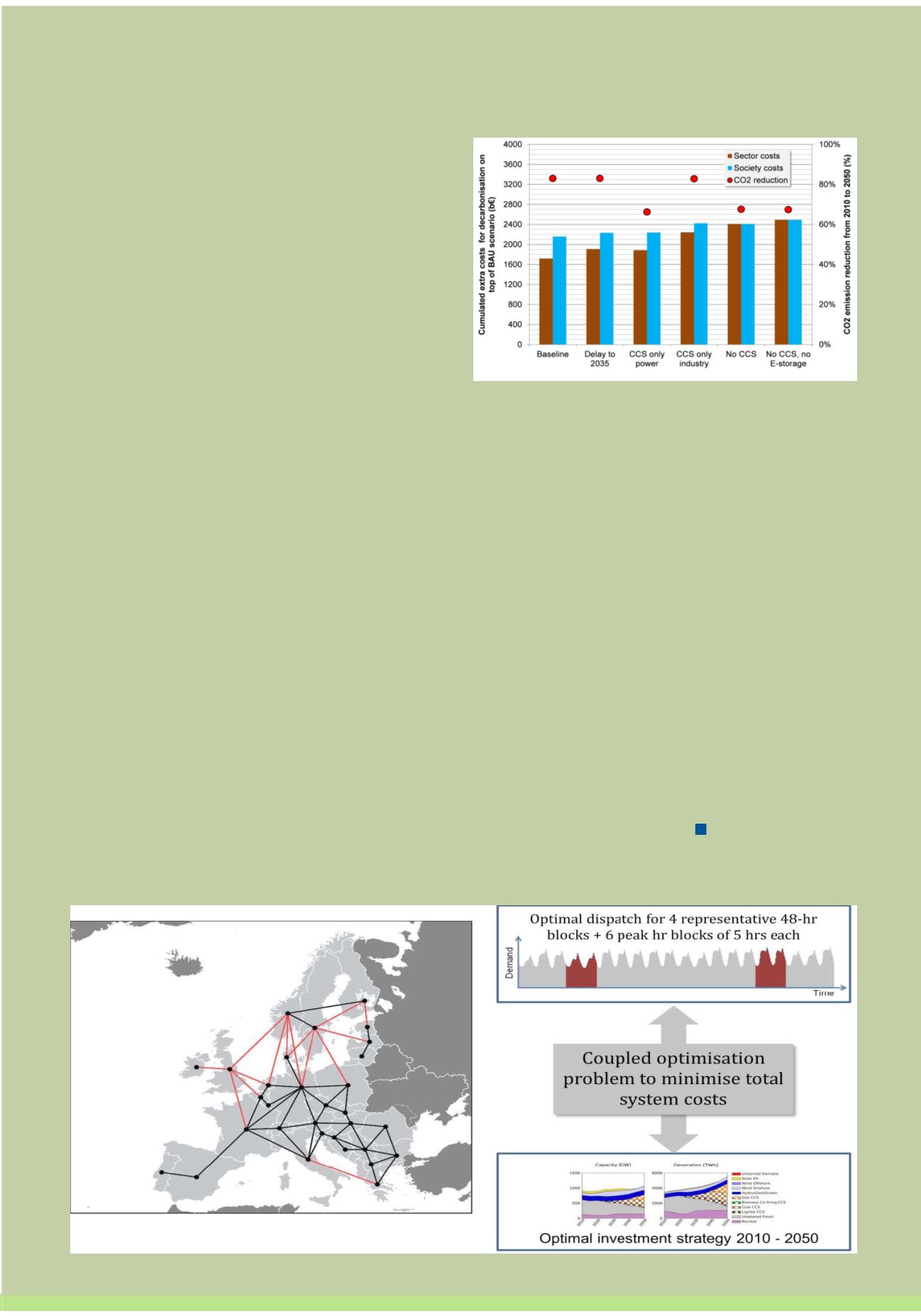

The reports key conclusions were:

• Energy-intensive industries account for a quarter of EU CO2

emissions and cannot reduce them substantially without

CO2 Capture and Storage (CCS).

• The absence of CCS support measures in the model

(upfront public investment in CO2 transport and storage +

incentives for energy-intensive industries) not only delays

CCS deployment to 2040, but leads to a CO2 reduction of

only 68% by 2050 – well below EU targets of 80-95% for

power and industry.

• Investment inCO2 transport and storage infrastructuremust

start now in order to deploy CCS widely from 2025 – a delay

of even 10 years will cost power and industry an extra €200

billion to reach these EU targets. It will also result in a forced

doubling of the annual CCS deployment rate to 15-20 GW

for power alone which is unrealistic given supply constraints

for the delivery of power plants, CCS infrastructure and the

necessary skills. Hence delaying CCS deployment until 2035,

while possible tomodel, risks severely limiting its optionality.

• When CCS is not part of the portfolio, the cost of reaching

the EU’s CO2 reduction target for power increases by at least

€1-1.2 trillion. The EU’s target for industry, on the other hand,

is not achievable – in any scenario.

Table 2: EMPIRE models the European countries generation capacities and import/export capacities between them.

Table 1: Extra cost of decarbonisation on top of Business as Ususal,

cumulated from 2010 to 2050 (flat electricity consumption).